Guilty of bookkeeping blunders? Our partners at Bench have compiled a list of the most common bookkeeping mistakes and how to avoid them.

Bookkeeping mistakes can put a big dent in your profits. Luckily, most of the really bad mistakes are easy to prevent. Here are the top 5 financial errors small business owners make, according to bookkeepers—and how you can avoid them.

![]() Table of Contents

Table of Contents

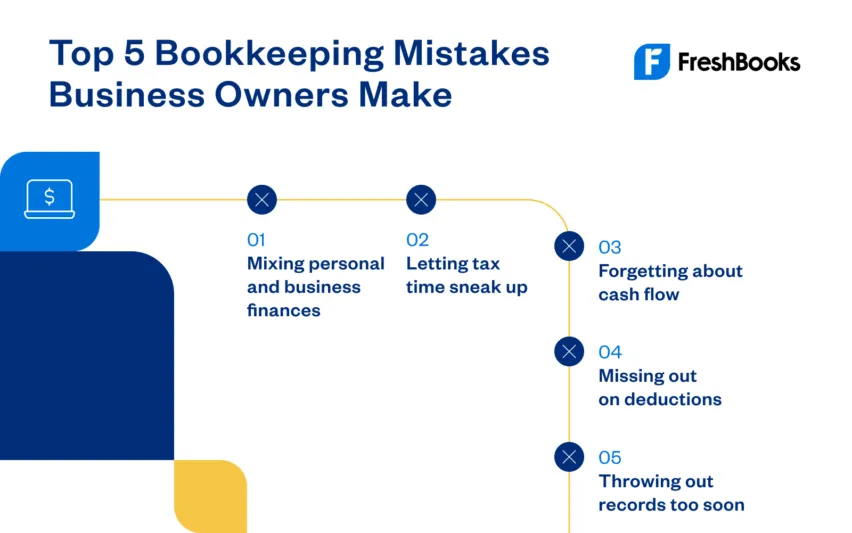

Mistake 1: Mixing Personal and Business Finances

At its heart, bookkeeping is all about tracking how money enters and leaves your business. That means recording and categorizing every transaction. It also means being crystal clear about which transactions are personal, and which ones are for your business.

Why Mixing Finances Is a Bad Move

When your personal and business finances are mixed together, it’s hard to tell where your expenses and income are coming from. In the end, that means more work for your bookkeeper as they try to figure out which transactions are personal, and which are business-related.

Example:

Let’s say you’re a freelance designer working from home. You use one credit card for all your personal and business transactions. One day, you go out and buy a brand new, ultra-ergonomic office chair.

5 Money Management Strategies Every First-Time Business Owner Should Know

5 Money Management Strategies Every First-Time Business Owner Should Know How to Stop Your Personal Money Habits From Affecting Your Business

How to Stop Your Personal Money Habits From Affecting Your Business Keeping It Professional: 3 Reasons Why You Need a Business Bank Account

Keeping It Professional: 3 Reasons Why You Need a Business Bank AccountWhen your bookkeeper sees that purchase on your credit card statement, they don’t know whether you bought the chair for use in your home office—in which case it should be recorded as an expense for your business—or for your den, where you play computer games in your downtime—in which case, it’s a personal expense.

Without an accurate record of your expenses, you don’t get a clear financial picture of how your business is performing.

Mixing finances can also mean you miss out on deductions. Let’s say you did buy that new chair for your office. In that case, it’s a tax-deductible business expense; by reporting it to the IRS, you can save money on taxes. But your bookkeeper may miss it if it’s mixed in with all your personal expenses—for instance, a new gaming PC you bought for your den.

Finally, miscategorizing transactions can get you in trouble with the IRS. Suppose your bookkeeper does record your new chair as a business expense, and you deduct it when you file taxes. But, because your transactions are all mixed together, they also record your new gaming PC as a business expense. In that case, you’re committing fraud—trying to claim a business deduction on personal expenses. In the event of an audit, you could land in hot water with the IRS.

How to Avoid It

Set up separate bank accounts for business and personal funds, and deposit all your business income in the business bank account. Get a business credit card and use it to make business purchases.

That way, your bookkeeper only needs to monitor your business accounts. It’s guaranteed that anything showing up on your statements must be recorded on your business books. No second-guessing, no mixed-up transactions.

Mistake 2: Letting Tax Time Sneak Up

Tax season comes at the same time every year. It shouldn’t be a surprise. But all too often, entrepreneurs leave taxes to the last minute. After slacking off on bookkeeping duties throughout the year, their books are in shambles. So, when the time finally comes to file, they’re left scrambling. Besides mental and emotional stress, this approach has some serious negative consequences.

Why Failing to Prep for Tax Time Is a Bad Move

First of all, if you file your taxes late or you file them incorrectly, the IRS can charge you penalty fees.

Plus, if your books are a mess come tax time, you don’t have a clear record of your expenses. That means you could miss out on deductions.

But one of the worst parts about failing to prepare for tax time is playing catch-up. Bookkeepers and accountants will charge you extra to get your books up to date for tax filing; that’s one more fee you must pay on top of taxes.

Also, if you don’t keep your books up to date throughout the year, you never have a clear picture of your business finances. So, when it’s time to make important decisions—how to spend your money or how to earn more of it—you won’t have good numbers to base them on.

If you don’t keep your books up to date throughout the year, you won’t have a clear picture of your business finances come tax time.

How to Avoid It

The first step is to know when your taxes are due. This can depend upon your business structure—such as whether you’re filing as a sole proprietorship or an S corporation.

Tax Return Deadlines:

- S-corporations and partnerships: March 15, 2023

- Individuals and sole proprietorships: April 18, 2023

- C corporations: April 18, 2023

Next, if you’re concerned you won’t have your tax return ready on time, prepare to file for a federal tax extension. It’s better to fill out the form and file the extension before you miss the due date, so you aren’t charged tax penalties.

Finally, if your books were disorganized last year when you filed, make a point this year of putting a bookkeeping solution in place. That could mean hiring a local bookkeeper or using an online bookkeeping service like Bench. When professionals handle your bookkeeping, you don’t have to worry about inaccurate or out-of-date books.

Whatever option you choose, make sure you’re able to get end-of-year financial statements—you’ll use them to calculate and file your taxes.

Mistake 3: Forgetting About Cash Flow

Cash flow measures how much money is coming into your business, how much you’re spending, and where it goes. When you don’t stay on top of cash flow, it gets hard to pay your bills on time.

Why Forgetting About Cash Flow Is a Bad Move

Didn’t track how much you owe this month? Unsure of how long it takes to get paid? Don’t know how many expenses your savings can cover in case of an emergency?

That’s what your books look like when you don’t track cash flow. You’re completely in the dark.

Suddenly, you may find yourself owing expenses you didn’t expect or coming up short when it’s time to pay. And that can cause serious damage to your financial well-being.

When your business is small and simple, you may get away with tracking cash flow haphazardly, just making sure you have enough to cover bills and pay yourself each month. But as it gets bigger and more complicated—your expenses and sources of income increase—you’ll find it’s hard to keep track.

How to Avoid It

The best defense against cash flow troubles is a solid bookkeeping system. Specifically, you need to make sure you’re getting monthly cash flow statements. Accounting software can handle this for you, provided you keep your books current. Otherwise, a professional bookkeeper can tackle the job.

Your best bet is to start tracking cash flow now. Even if your business is small, you’ll get a clear picture of your financial standing. And you’ll be prepared if or when your business becomes bigger and more complex.

Mistake 4: Missing Out on Tax Deductions

A lot of the money you spend to stay in business can be deducted from your taxes. For instance, if you use part of your home as an office, you can deduct a corresponding portion of your rent or property taxes. If you use your phone to make business calls, you may be able to deduct some of the bill. And even a casual business meeting in a coffee shop can mean writing off the cost of 2 cappuccinos.

Why Missing Out on Deductions Is a Bad Move

The more deductible expenses you report to the IRS, the lower your tax liability. That’s less income you have to withhold for taxes. In a way, tax deductions are free money: You’re legally entitled to them; all you have to do is make sure they’re correctly recorded and reported.

5 Reasons Why Business Expense Tracking Is Important

5 Reasons Why Business Expense Tracking Is Important Guide to U.S. Tax Write-Offs for Small Business Owners

Guide to U.S. Tax Write-Offs for Small Business Owners A Must-Read U.S. Small Business Tax Checklist

A Must-Read U.S. Small Business Tax ChecklistOne of the main reasons self-employed people miss out on deductions is that they don’t have a system in place to track them.

You may have started your freelance business as a side hustle before the business gradually grew and you quit your day job to do it full time. Then, before you knew it, tax season came along, and you had no idea what expenses you had incurred, and which ones you could report on.

The other reason freelancers miss out? They opt for a standard deduction rather than itemized one. You may have always claimed a standard deduction on your personal taxes. But now that you’re in business, the standard deduction may be the less lucrative option.

How to Avoid It

Up-to-date, accurate books keep track of all the money you spend in the course of doing business. The books are your first stop when it’s time to determine what you can deduct.

You’ll need receipts to back up those claims, though. In that case, FreshBooks’ expense tracking tool lets you photograph every proof of purchase and record it as an expense.

Finally, enrolling the help of an accountant is key. They can let you know whether you should be opting for itemized or standard deductions in order to save the most money. And they can help you figure out which expenses you can report to the IRS, and which you can’t.

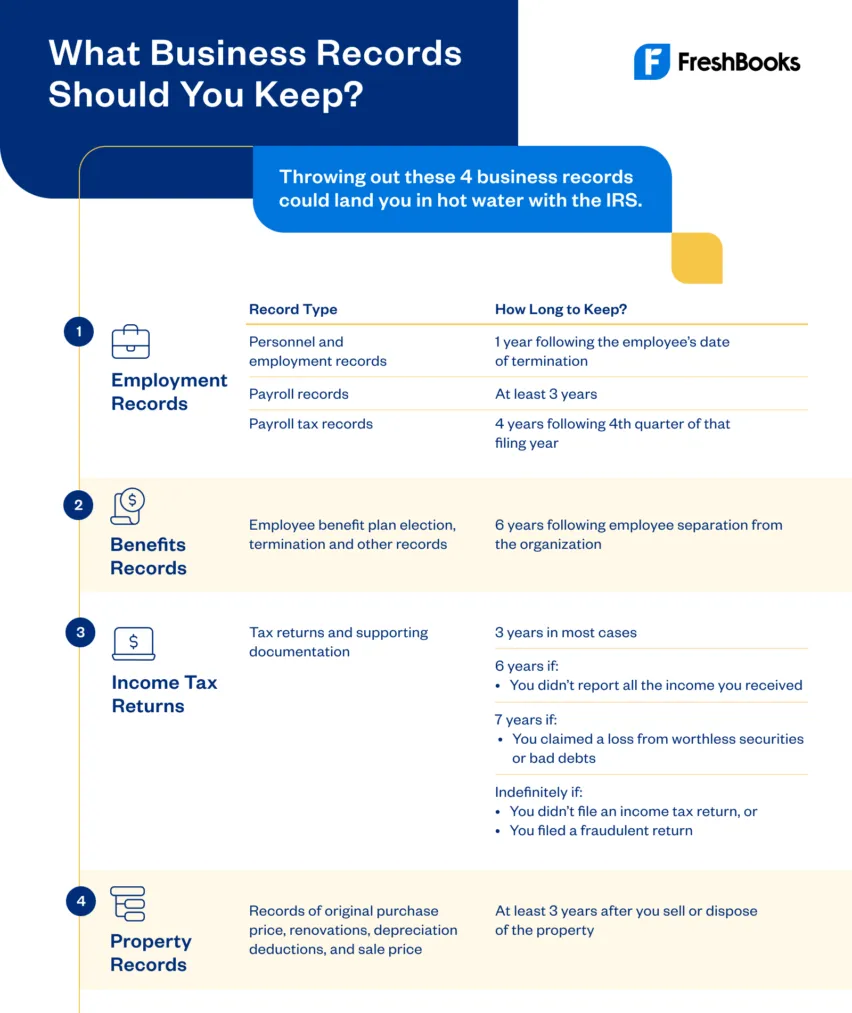

Mistake 5: Throwing Out Financial Records Too Soon

When tax season is past, and it’s time for spring cleaning, you may be tempted to ditch many of your old business records. But before you do, know which ones you must hold on to for tax purposes.

Why Throwing Out Records Too Soon Is a Bad Move

If the IRS audits you, and you don’t have the records you need to back up deductions you’ve claimed on past tax returns, they could penalize you.

Even if your chances of being audited are slim, it’s good practice to hold on to every tax record. The effort is very little relative to the trouble you could run into if you don’t.

How to Avoid It

Hold on to every receipt—preferably with help from an online solution like the FreshBooks’ expense tracker, which scans receipts and automatically organizes them by expense category.

And remember this: Keep every record for at least 3 years.

Why? The period of limitations on your tax return is 3 years. During those 3 years, you’re able to amend your return. And the IRS can audit you.

So, if you have records for your 2023 tax return, hold onto them until you’ve filed your return for 2027.

There are some exceptions to this:

- Employment records for people on your payroll: Save records for 4 years

- Employee benefit records: Save for 6 years after the employee leaves the company

- Returns (and supporting documentation) where you omitted more than 25% of your gross income: Save for 6 years after you’ve filed or after the due date of the return (whichever is longest)

- Records for the cost of bad debt or worthless securities you deducted on your tax return: Save records for 7 years after you filed or the due date of the return (whichever is longest)

- Supporting documentation for returns you failed to file or for fraudulent returns: Save records indefinitely

For a more detailed rundown of how to keep business records, check out Bench’s guide to how long to keep business tax records.

Get Help With Your Small Business Bookkeeping

Many small business owners start out doing their own bookkeeping. But as you grow, you may want to consider hiring an experienced bookkeeper or accountant to help at tax time or with financial reports and planning year-round. Learn how Bench and FreshBooks can help.

This post was updated in February 2023.

Written by Bryce Warnes, Writer, Bench Accounting

Posted on December 23, 2022

Freshly picked for you

How to Find the Right Small Business Accountant to Support Your Growth

How to Find the Right Small Business Accountant to Support Your Growth

A Beginner’s Guide to Financial Statements

A Beginner’s Guide to Financial Statements

An Easy Solution to Organized U.S. Taxes: Business Expense Categories

An Easy Solution to Organized U.S. Taxes: Business Expense Categories

Partner News: Stay on Top of Your Books With Bench Bookkeeping Services

Partner News: Stay on Top of Your Books With Bench Bookkeeping Services

![How to Choose the Right Bookkeeping Service [Free Checklist]](https://www.freshbooks.com/blog/wp-content/uploads/2018/10/Checklist-Hero@2x-226x150.jpg) How to Choose the Right Bookkeeping Service [Free Checklist]

How to Choose the Right Bookkeeping Service [Free Checklist]

Graham (Self-Proclaimed Tax Nerd) Saves 44 Hours a Year on Tax Prep Using FreshBooks

Graham (Self-Proclaimed Tax Nerd) Saves 44 Hours a Year on Tax Prep Using FreshBooks